Assets & Liabilities Explained

It’s no secret running your own business comes with a host of responsibilities so it’s easy to see why the ins and outs of your finances can often get pushed aside.

However, understanding your assets and liabilities is crucial. They are the main parts of the Balance Sheet for your business and will help you understand how healthy important parts of your business are.

Assets & Liabilities: what’s the difference?

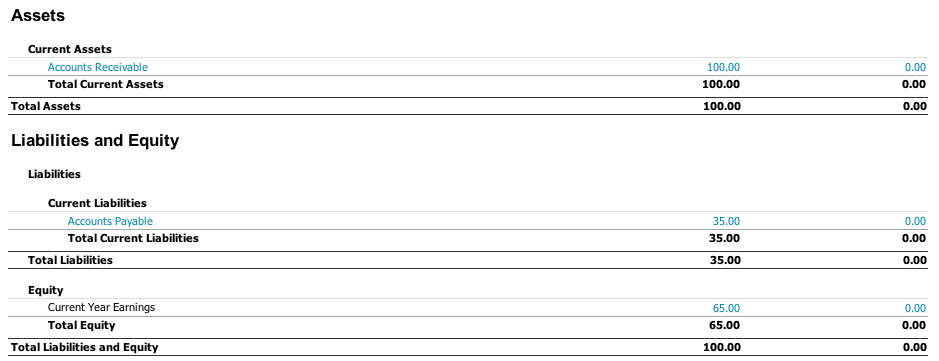

Assets refer to the ‘green’ of your business. Basically, things you own that have a future financial benefit. So assets owned by the business like cash in the bank, computers, cars, accounts receivable and more. There are some non-tangible (physical things) also, but we’ll keep it simple here.

Liabilities refer to what your business owes aka the ‘red’ in your business. For example, tax debts, business loans, wages not yet paid (+ leave, super etc) and money owed to others.

When you add up your assets and minus your liabilities you end up with the equity you have in the business. This is known as a balance sheet. You have yourself a clear understanding of where your business sits financially – the more your assets exceed your liabilities, the healthier your business is. On the flip side, if you end up with more liabilities than assets, well you’re not in a great place.

How to interpret your assets and liabilities

It’s all well and good to cast your eye over your assets and liabilities but having a deep understanding of them is important.

The main reasons?

- To ensure you’re financially capable of paying your bills

- To check your stock levels

- To manage your debt

- To understand your financial position

Once you’ve got this down pat, you can confidently invest/spend where you need to, increase staff support or if needed, move stock to increase cash and curb some expenses. You can use this information to help form long term business plans and even pivot quickly where needed.

On the flip side, imagine you make a big purchase only to find out a big debt is looming? Cue mad scrambling to make it work! You don’t need that kinda stress so keeping on top of your assets and liabilities is a must.

Long term health checks

Now that you have a solid grasp of your assets, equity and liabilities, it’s time to chat more about your balance sheet. Your balance sheet is the report bringing this all together, telling you how much your business owns vs how much it owes: aka your assets and liabilities.

To keep this balance sheet working for you, it must be reconciled. As much as you’d love it to correct and adjust itself, there is always room for human error. Make a date with yourself and/or your bookkeeper to check on:

- Stock levels – ensuring they match what’s in your system (assets)

- Bank statements – checking income, expenditure and balances

- Debtors – chasing owed money and cleaning up your files

Our clients never get a balance sheet unless it’s been reconciled because these figures directly impact your profit and loss report. One stray error and all reports will be blown out.

And there you have it, the ins and outs of your assets and liabilities. Keeping your finger on the pulse really is key to maintaining a healthy cash flow. Inconsistent cash flow? Read This.

Need more help? Reduce the overwhelm, learn how to understand and have confidence in your numbers with me.